JobKeeper 2.0 from 28 September 2020

From 28 September 2020, the eligibility tests to access JobKeeper for employers will change, as will the amount of the JobKeeper payment for employees and business participants. To receive JobKeeper from 4 January 2021, employers will need to assess their eligibility again.

Eligibility for one JobKeeper period does not entitle you to, or exclude you from, payments in another period. Each eligibility period is addressed separately. That is, there might be businesses that qualified for the first tranche of JobKeeper, don’t qualify for the second tranche but qualify for the third.

1. Eligible businesses

Eligible employers

An eligible employer is an employer that:

· On 1 March 2020, carried on a business in Australia or was a non‑profit body pursuing its objectives principally in Australia; and

· before the end of the JobKeeper fortnight, it met the original decline in turnover test*:

· And, was not:

o on 1 March 2020, subject to Major Bank Levy for any quarter ending before this date, a member of a consolidated group and another member of the group had been subject to the levy; or

o a government body of a particular kind, or a wholly-owned entity of such a body; or

o at any time in the fortnight, a provisional liquidator or liquidator has been appointed to the business or a trustee in bankruptcy had been appointed to the individual’s property.

1 March 2020 is an absolute date. An employer that had ceased trading before 1 March, commenced after 1 March 2020, or was not pursuing its objectives in Australia at that date, is not eligible.

*Additional tests apply from 28 September 2020.

Business owners

Business owners:

· sole traders with an ABN, and

· one partner in a partnership, adult beneficiary of a trust, director or shareholder who works in the business (i.e., only one person in a partnership, one beneficiary of a trust, or one director / shareholder are eligible for JobKeeper payments).

will be eligible for the JobKeeper payment if the following conditions are met:

· The entity carried on a business on 1 March 2020 and is not a not-for-profit entity; and

· Had an ABN on 12 March 2020; and

· Had some business income in the 2018-19 income year included in a tax return that was lodged by 12 March 2020; or made some supplies connected with Australia in a tax period that started on or after 1 July 2018 and ended before 12 March 2020 and notified the ATO of this (e.g. on an activity statement lodged with the ATO) by 12 March 2020. The Commissioner can potentially extend the deadline for holding an ABN, lodging the 2019 tax return or lodging a relevant activity statement.

· Passed the decline in turnover test; and

· The individual was not:

o employed by the business at any time in the relevant fortnight; or

o a permanent employee of another entity at the time the individual gives the nomination notice (i.e., they do not hold a full time or part time role with another employer); or

o a nominated JobKeeper employee of any other business; or

o entitled to parental leave pay or dad and partner pay or workers’ compensation payments for being totally incapacitated for work.

As at 1 March 2020, the individual satisfied all of the following:

o Aged 16 years or over; and

o If they are aged 16 or 17 years, they are either financially independent or are not undertaking full-time study;

o Actively engaged in the business; and

o An Australian resident under the Social Security Act or an Australian tax resident who holds a special category visa **

If the criteria have been met, the individual is eligible if they were actively engaged in the business in the fortnight of the JobKeeper payment, and they agreed to be nominated for JobKeeper payments and confirmed they pass the eligibility criteria.

What about the directors who work in the business?

If more than one director wants to access JobKeeper payments, they need to meet the eligibility criteria of an employee (see Eligible employees). To be an employee a director would have received salary/wages and this has been reported as salary/wages on activity statements, payment summaries, tax returns etc. If a director merely receives a distribution from the business then they are unlikely to be an employee.

The decline in turnover test

For businesses already enrolled in JobKeeper, to receive payments from 28 September 2020, you need to meet an extended decline in turnover test based on actual GST turnover.

Businesses that are enrolling for the first time, need to meet the basic eligibility test and the decline in turnover test/s for the relevant period.

* Alternative tests may apply

Most businesses will generally use their Business Activity Statement (BAS) reporting to assess eligibility. However, as the BAS deadlines are generally not until the month after the end of the quarter, eligibility for JobKeeper will need to be assessed in advance of the BAS reporting deadlines to meet the wage condition for eligible employees.

The ATO has the power to extend the time an entity has to pay employees in order to meet the wage condition. For the JobKeeper fortnights starting 28 September 2020 and 12 October 2020 the ATO is allowing employers until 31 October 2020 to meet the wage condition for all employees included in the JobKeeper scheme.

Calculating GST turnover

Calculating GST turnover for tranches 2 and 3 of JobKeeper is different to the original JobKeeper requirements as entities will only be using current GST turnover figures (not projected GST turnover).

When applying the new turnover reduction tests for the September 2020 quarter and December 2020 quarter, entities that are registered for GST must use the same method that is used for GST reporting purposes. That is, if the entity is registered for GST on a cash basis then a cash basis needs to be used to calculate current GST turnover for the purpose of these new tests. Entities that are not registered for GST can choose whether to calculate GST turnover using a cash or accruals basis, but must use a consistent method.

Current GST turnover includes proceeds from the sale of capital assets, unless the sale is input taxed. Current GST turnover includes taxable and GST-free supplies, but should exclude input taxed supplies such as residential rental income and financial supplies like dividends, interest etc. JobKeeper and ATO cash flow boost payments should be excluded from the calculation along with other payments that don’t represent consideration for a supply made by the entity such as certain State based grants.

What if you don’t have a comparison period or there was a one-off event?

The Commissioner of Taxation has the power to set out alternative tests that establish eligibility in specific circumstances where it is not appropriate to compare actual turnover in a quarter in 2020 with actual turnover in a quarter in 2019. The Commissioner provided a number of alternative tests that could be used for passing the original decline in turnover test and the ATO has indicated that similar tests are likely to be available for the additional decline in turnover tests for the September 2020 and December 2020 quarters, but these have not been released as yet.

Not for profits

A number of modifications apply to not for profit entities when it comes to calculating GST turnover under the original decline in turnover test. It appears that the same modifications will generally also apply when determining whether a not for profit entity passes the new decline in turnover tests for the September 2020 and December 2020 quarters.

Wage condition

To be eligible to receive JobKeeper payments, the employer must meet a wage condition. That is, employers must have paid the eligible employee at least the applicable JobKeeper payment for the relevant fortnight.

The ATO reimburses the employer for the JobKeeper payment monthly in arrears.

As noted above, for the JobKeeper fortnights starting 28 September 2020 and 12 October 2020 the ATO is allowing employers until 31 October 2020 to meet the wage condition for all employees included in the JobKeeper scheme.

2. Eligible employees

From 3 August 2020, the eligibility tests for employees were changed to enable a greater number of employees to access JobKeeper.

Previously, an employee had to be employed by the relevant entity on 1 March 2020 to be eligible for JobKeeper payments. Someone employed as a casual on that date also must have been employed on a regular and systematic basis for the 12 month period leading up to 1 March 2020.

Now, employees who were previously ineligible for JobKeeper because they were not employed by the entity on 1 March 2020 may be able to receive JobKeeper payments if they were employed by the entity on 1 July 2020 and can fulfil all of the other eligibility requirements. If an employee already passed all the relevant conditions at 1 March 2020 then they don’t need to be retested using the 1 July 2020 test date.

· On 1 July 2020 (previously 1 March 2020):

· Was aged 16 years and over; and

· If the individual was aged 16 or 17, was either financially independent or was not undertaking full-time study;

· Was an employee other than a casual, or was a long-term casual*; and

· Was an Australian resident (under the meaning of the Social Security Act 1991), or a resident for tax purposes and held a Subclass 444 (Special category) visa**.

· And, at any point during the JobKeeper fortnight:

· Was an employee of the employer (including employees that have been stood down or rehired); and

· Was not an excluded employee:

§ An employee receiving parental leave pay or dad and partner pay; or

§ An employee receiving workers compensation payments in relation to total incapacity.

· And, has provided the JobKeeper Payment Employee Nomination to the employer:

· Agreeing to be nominated by the employer as an eligible employee under the JobKeeper scheme; and

· Confirming that they have not agreed to be nominated by another employer; and

· If they are a long-term casual, they do not have permanent employment with another employer.

*A ‘long term casual employee’ is a person who has been employed by the business on a regular and systematic basis during the period of 12 months that ended on the applicable testing date (previously 1 March 2020, but changing to 1 July 2020). These are likely to be employees with a recurring work schedule or a reasonable expectation of ongoing work.

3. JobKeeper payments

From 28 September 2020, the payment rate for JobKeeper will taper from the flat rate of $1,500 and split into a higher and lower rate.

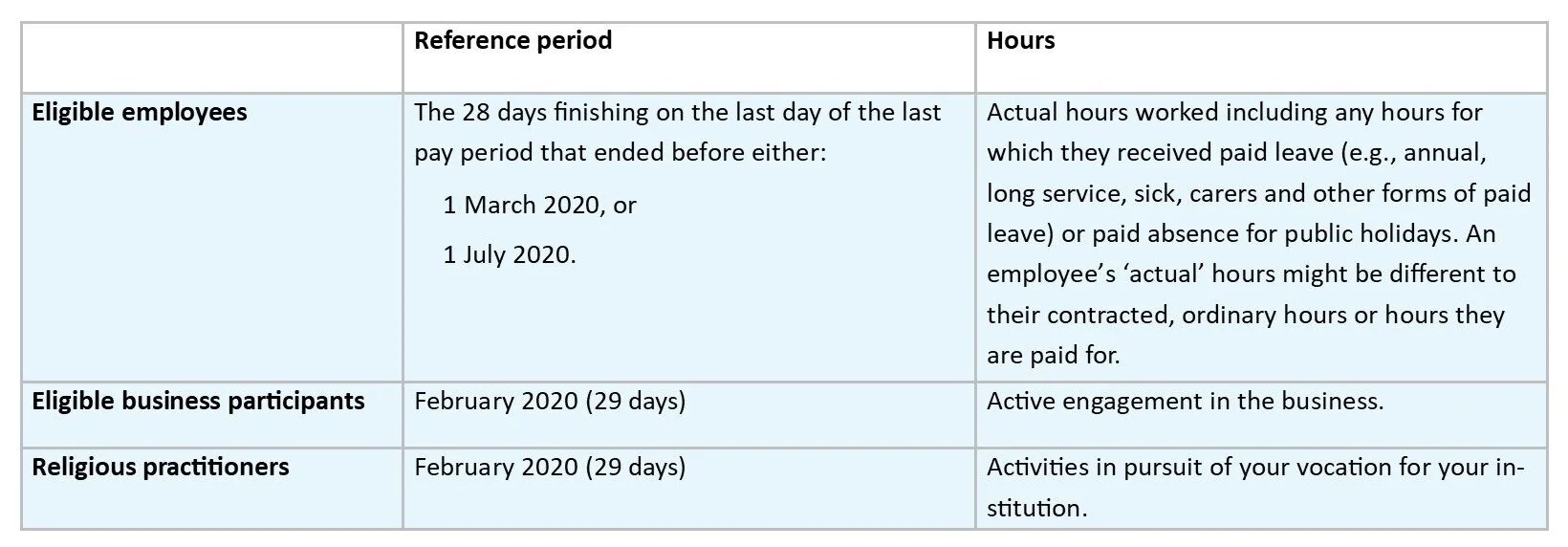

What’s a reference period?

Eligible employees

Eligible employees that have been employed on a full time basis since 1 March 2020 or 1 July 2020 will generally receive the higher JobKeeper rate (as full time employees work more than 80 hours in 28 days) .

Businesses however will need to determine the rate applicable to eligible part-time and casual employees.

The reference period is the 28 day ending at the end of the most recent pay cycle for the employee ending before:

· 1 March 2020; or

· 1 July 2020.

For eligible employees who have been employed since 1 March 2020, employers need to choose the reference period that provides the best outcome for the employees. For many employers, this will be the pre COVID-19, 1 March 2020 reference date.

For eligible employees employed since 1 July 2020, use the pay periods prior to 1 July 2020.

If the pay cycle is longer than 28 days, a pro-rata calculation needs to be done to determine the average hours worked and on paid leave across an equivalent 28 day period. For example, if the relevant monthly pay cycle has 31 days, you take the total hours for the month and multiply this by 28/31.

In order for an employer to receive JobKeeper payments from 28 September 2020 onwards they must notify the ATO of the payment rates for all eligible employees. The employer must then notify its employees within 7 days of advising the ATO of the payment rate.

What happens if the reference period does not represent the employee’s typical arrangements?

Alternative tests are available where:

· There reference period is not typical of the employee’s hours or you use a rostering system and there is no typical pattern in a 28 day period; or

· The employee started work during the reference period.

Reference period not typical

Where the reference period is not typical of an employee’s hours, for example they took unpaid leave, or your business was in a drought or bushfire zone, or the employee was stood down etc., you can use an earlier 28 day period or multiple 28 day periods that more accurately represent the employee’s typical arrangements.

The reference period becomes the 28 day period ending at the end of the most recent pay cycle for the employee before 1 March 2020 or 1 July 2020 in which the employee’s total number of hours of work, of paid leave and of paid absence on public holidays was representative of a typical 28-day period. That is, you select the next 28 day period before 1 March 2020 or 1 July 2020 that represents the employee’s typical employment pattern.

For workers that don’t have a typical pattern because of a rostering system like fly-in-fly-out workers, an average of the hours worked over the employee’s rostering schedule and proportionally adjusted over 28 days can be used to work out a typical 28-day period.

Employee started work during the reference period

Where an employee started work during the 28 days prior to either 1 March 2020 or 1 July 2020, you can use a forward-looking alternative test. In these circumstances, use the pay cycle immediately on or after 1 March 2020 or 1 July 2020. For employers with fortnightly or weekly pay cycles, you must use consecutive weeks.

Where an employee was stood down, use the first 28 day period starting on the first day of a pay cycle on or after 1 March 2020 or on or after 1 July 2020 in which they were not stood down.

Sale of business or changes within a group

Where the business changed hands or the employee changed employment within a wholly owned group, the hours worked with the previous employer cannot be counted. Instead, use the pay cycle immediately on or after 1 March 2020 or 1 July 2020. For employers with fortnightly or weekly pay cycles, you must use consecutive weeks.

If the employee has been stood down, use the first 28 day period starting on the first day of a pay cycle on or after 1 March 2020 or on or after 1 July 2020 in which they were not stood down.

What happens if employee salary is not linked to hours?

Some employees will automatically qualify for the higher JobKeeper payment rate. Broadly, this applies if the employer has incomplete records of total hours of work and paid leave, including where salary, wages, commissions, bonuses etc are not tied to an hourly rate or contracted rate.

The employee must also fall within specific categories, including:

· They were paid at least $1,500 in the reference period;

· They were required to work at least 80 hours under an industrial award, enterprise agreement or contract; or

· It is reasonable to assume that they worked at least 80 hours during the applicable period.

Business owners and sole traders

The reference period for business participants is the month of February 2020 (the whole 29 days).

A business participant is a sole trader or self-employed with an ABN, or one partner in a partnership, adult beneficiary of a trust, director or shareholder who works in the business (i.e., only one person in a partnership, one beneficiary of a trust, or one director / shareholder can be eligible for JobKeeper payments for a particular entity).

The test to determine eligibility is based on the hours of active engagement in the business carried on by the entity. This requires an assessment of the hours that the business participant was actively operating the business or undertaking specific tasks in business development and planning, regulatory compliance or similar activities in an applicable reference period.

Other than sole traders and self-employed, a business participant must provide a declaration to the business entity confirming their hours worked over the reference period.

For JobKeeper payments from 28 September 2020, the business must notify the Tax Commissioner about whether the higher or lower rate applies to the business participant and notify the participant within 7 days of providing this notice to the Commissioner.

Where February 2020 was not typical of the participant’s hours, an alternative test can be used:

· Not typical - use the next typical 29 day period

· Commenced work during February 2020 – use March 2020

· Not employed by the employer but still an eligible religious practitioner for JobKeeper purposes - use March 2020

Religious practitioners

The reference period for eligible religious practitioners is the month of February 2020.

A religious practitioner is a minister of religion or a full time member of a religious order who undertakes activities in pursuit of their vocation as a member of a religious institution.

The payment rates are based on the number of hours they spent doing an activity, or series of activities, in pursuit of their vocation as a religious practitioner as a member of the religious institution in the reference period. For example:

· Performance of the rituals or practices of the religious institution (including participation in services, prayer, contemplation or meditation, insofar as they constitute such rituals or practices); and

· Furtherance of the objectives of the religious organisation (including missionary or charitable work, insofar as they constitute such an objective).

The religious practitioner must provide a declaration to their institution confirming their hours worked over the reference period.

For JobKeeper payments from 28 September 2020, religious institutions must notify the Tax Commissioner about whether the higher or lower rate applies to each of their eligible religious practitioners and notify the practitioner within 7 days of providing this notice to the Commissioner.

Where February 2020 was not typical of the practitioner’s hours, an alternative test can be used:

· Not typical - use the next typical 29 day period

· Commenced work during February 2020 – use March 2020

· Not employed by the employer but still an eligible religious practitioner for JobKeeper purposes - use March 2020